Division 296: A new era for superannuation taxation

October 22, 2025

For Australia’s wealthiest investors, the landscape of superannuation is about to shift dramatically. The proposed new Super tax, Division 296 – officially known as the Better Targeted Superannuation Concessions Tax (BTSC tax) – is poised to reshape how high-balance superannuation accounts are taxed, with significant implications for retirement planning, estate strategies, and overall wealth management.

While the Federal Government’s update on 13 October scrapped the tax on unrealised gains and introduced indexation, which was welcomed by many, the new 40% tax on balances over $10 million will still have significant impacts on high Super balances.

Many questions also remain for investors, such as whether existing superannuation assets will be grandfathered. If the answer is no, with many Australians holding property and shares within their superannuation, many more are set to be impacted by the $3 million Super tax.

What is Division 296?

Set to take effect from 1 July 2026 – a year later than the Government originally planned – Division 296 will introduce a tiered tax structure targeting individuals with superannuation balances exceeding $3 million:

- Balances between $3 million and $10 million: Earnings will be taxed at 30%, which is an additional 15% above the current rate.

- Balances over $10 million: Earnings will be taxed at 40%, which is an additional 25% above the current rate.

This tax is personal, not levied on the super fund itself, and applies to both public funds and self-managed super funds (SMSFs). Importantly, it only targets realised earnings such as dividends, interest, rent, and realised capital gains.

Timeline and implementation

Assuming the legislation passes, the first Division 296 assessments will be based on earnings during the 2026–27 financial year, with tax payments due from 1 July 2027. The thresholds will be indexed annually, with the $3 million cap increasing in $150,000 increments, while the $10 million cap will increase in $500,000 increments.

What could this mean for you?

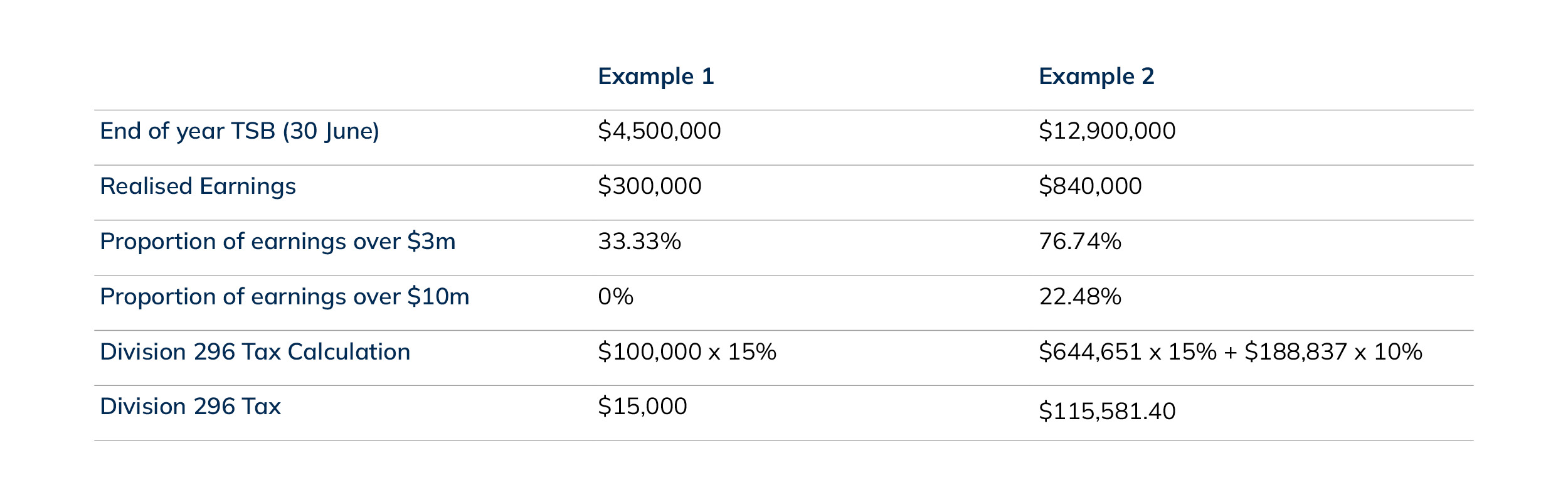

Let's consider two hypothetical retirees:

These figures are in addition to existing Super fund taxes. For investors with substantial balances, the impact could be significant.

Want to learn how much you may have to pay? Click here to use the Ord Minnett Division 296 Tax Calculator.

What's still to be determined

While the broad framework of Division 296 is now public, several critical details remain under consultation.

- Treasury has yet to confirm the precise method for calculating and attributing realised earnings to in-scope members, particularly regarding the treatment of capital gains and the CGT discount. Notably, there are no transitional provisions addressing how capital gains accrued before the start date will be treated if realised after commencement e.g. “grandfathered” assets.

- The treatment of negative earnings and capital losses is also unresolved and will be clarified through ongoing design discussions.

- For defined benefit interests, further consultation will determine how these are valued and when the tax will apply.

- Additionally, the mechanisms for reporting earnings and paying the tax – both for individuals and superannuation funds – are still being finalised.

Strategic responses to consider

While some may consider withdrawing funds to reduce their balance below the $3 million threshold, this could trigger capital gains tax or higher personal tax rates. Other strategies include:

- Alternative structures: Investing via family trusts or companies (taxed at 25% for eligible entities).

- Gifting to adult children: A tax-effective way to transfer wealth.

- Investing in your Principal Place of Residence (PPOR): Renovations or upgrades may offer better long-term value.

Each option carries its own risks and benefits. The key is personalisation – what works for one investor may not suit another.

The bottom line: seek advice

Division 296 isn’t just another tax tweak - it’s a fundamental shift in how Australia treats high-value retirement savings. With more than $71 billion* in Funds Under Advice, firms like Ord Minnett are already helping clients navigate this new terrain.

Before making any decisions – especially withdrawals or structural changes – speak with your private wealth adviser. The right strategy could mean the difference between a manageable tax bill and a costly misstep.

If you’re ready to start a conversation with Ords today and you’re not yet a client, click here to leave your details and an adviser will be in touch for an initial conversation.

*Figures as at 30 June 2025

Important Information

This webpage provides general information only and does not constitute financial, investment, or tax advice, and should not be relied on take make financial, investment or taxation decisions. The information is based on proposed legislation and current publicly available information as of October 2025, which may be subject to change. Individuals should seek professional advice tailored to their specific circumstances before making any decisions

Insights that count

Discover the best opportunities to outperform the market. Our research team dig deep into the market, company and stock data to bring you insights others might overlook.

Ord Minnett partnership gives firm something to Crow about

Ord Minnett (Ords) has partnered with the Adelaide...

AFR: Ord Minnett eyes bigger slice of small-cap equities, hires analysts

Ord Minnett’s Alastair Hunter and Angus Esslemont spoke to the...

Forbes: The Aussie Dollar Is Falling: Should Your Investments Change?

The Australian dollar has been weakening in 2023 and sits at US64...

.jpg)